9 Financial Data Compliance Challenges Banks Must Solve in 2026

For decades, banks have struggled to trace how regulated numbers are produced across borders, systems, and teams. What's changed in 2026 isn't the problem itself. It's the scale and speed at which regulators expect answers. Below is a practical walk-through of the toughest challenges and what "good" looks like when you tackle them with metadata, lineage, and accountable ownership at the core.

Your compliance officer just received her morning regulatory alert digest: 257 new or amended regulatory obligations across the financial services sector today. Not this month, today. While she processes that deluge, your stress testing team is assembling evidence packages covering capital plans and risk models across dozens of systems, your data protection team is responding to subject access requests spanning 15 different platforms, and your audit committee wants to know: "Can you prove where this capital adequacy number came from?"

Welcome to 2026, where regulatory complexity isn't slowing down, but accelerating. European banks face DORA enforcement requirements for ICT resilience, T+1 settlement deadlines compressing trade processing timelines, the EU AI Act's high-risk obligations taking effect in August, and ongoing Basel III/CRR capital requirements. The existential question: can manual processes, spreadsheets, and email chains keep pace with hundreds of daily regulatory changes?

The answer is no. Here are nine compliance challenges that will define 2026 for banks and why automated data lineage, unified business glossaries, and clear data ownership are no longer optional.

1. Inconsistent Data Definitions Across Regulatory Reports

European banks must produce hundreds of regulatory reports annually: Basel III/CRR capital calculations, MiFID II transaction reporting, GDPR data protection disclosures, and DORA operational resilience documentation. Each report may require different definitions, calculations, and data cuts from the same underlying systems.

The problem in practice:

Your CRM system defines "active customer" as anyone with activity in the last 90 days. Your risk management system uses 180 days. Your marketing platform uses 30 days. When producing a regulatory report on customer exposure or calculating capital requirements, which definition is correct?

Without a unified business glossary that maps how each term is defined across systems and which definition applies to which regulatory context, your teams spend weeks manually reconciling data. One bank reported needing over 1,000 employees just to prepare quarterly regulatory submissions because data definitions weren't standardized.

The regulatory stakes:

GDPR violations alone trigger fines up to €20 million or 4% of global annual turnover, whichever is higher. British Airways faced a £183 million penalty (later reduced) for a 2018 data breach; Marriott was fined £99 million for inadequate data security. Beyond fines, inconsistent definitions undermine the accuracy of capital calculations, risk assessments, and compliance reporting.

A centralized business glossary where terms like "customer," "transaction," "exposure," and "counterparty" have documented definitions, with explicit mappings showing which definition applies in which regulatory context (Basel vs. MiFID vs. GDPR). When definitions conflict, the system flags it before reports are submitted, not after regulators question your numbers.

2. The BCBS 239

The Basel Committee issued BCBS 239 principles for risk data aggregation in 2013, requiring "timely, accurate aggregation" of risk data with complete traceability. Yet BCBS 239 standards have been around for over a decade, yet most global banks still struggle with basic compliance because their data lives in systems that can't talk to each other.

When regulators ask, "How was this risk-weighted asset calculated?" can your team trace it back to source transactions in minutes, or does it require weeks of investigation? You need to provide the lineage of those numbers with audit-grade documentation.

3. 257 Daily Regulatory Changes

Thomson Reuters Regulatory Intelligence tracked organizations facing an average of 257 regulatory change events every business day. By 2022, that figure reached 234 alerts daily from 1,300+ regulatory bodies, over 61,000 alerts annually.

Each change potentially impacts data definitions, retention requirements, reporting formats, or control procedures. Manual processes don’t work for compliance anymore. Spreadsheets and email chains weren't designed for this level of complexity. When a MiFID II amendment changes transaction reporting fields, how quickly can you identify which systems, transformations, and reports are affected?

Organizations need impact analysis capabilities, like a data lineage. If a regulatory definition changes, instantly see which data sources, business rules, and downstream reports require updates.

4. Audit-Grade Data Lineage

Meeting each regulatory requirement can be a massive undertaking. Major banks must manage thousands of regulatory reports, requiring thousands of employees to reconcile data manually due to poor data flow visibility and fragmented data ecosystems.

European stress testing programs exemplify this complexity. Banks must document capital planning processes, stress testing methodologies, model validation procedures, data lineage for all calculations, and risk aggregation frameworks, all while maintaining audit-ready evidence that regulators can verify.

Multiply that documentation burden across dozens of regulatory submissions annually: Basel III/CRR capital calculations, ECB stress testing (SREP), MiFID II transaction reporting, GDPR data protection impact assessments, DORA operational resilience documentation, and jurisdiction-specific requirements.

Regulators want end-to-end lineage: which source systems fed this calculation, what transformations were applied, who approved the business logic, when did data quality checks run, and how do you ensure completeness? Manual documentation becomes obsolete the moment business processes change.

5. Fragmented Customer Data Across CRM, Trading, and Risk Systems

Your CRM tracks customer relationships. Your trading platforms record counterparty exposures. Your risk systems model credit and operational risk. Your core banking systems handle deposits and loans. Missing, outdated, or siloed data can compromise strategic decision-making. Each system defines "customer" differently, uses distinct identifiers, and maintains separate data quality standards.

When regulators request consolidated customer exposure reports or anti-money laundering investigations, teams spend weeks just understanding where customer data exists and how different systems define the same concepts. Is "ABC Corporation" in your CRM the same entity as "ABC Corp" in your trading system? Which system holds the authoritative view?

Without a data catalog that maps where customer data lives across your organization and how each system defines key entities, teams can't even begin reconciliation. They don't know which systems to check, which definitions apply to which regulatory context, or who owns each data source.

A data catalog that provides complete visibility: which systems store customer data, how each defines "customer" or "counterparty," which attributes exist where, and who is responsible for data quality in each system. When regulators request customer exposure reports, your team immediately knows which systems to query and how to interpret the results, cutting investigation time from weeks to hours.

6. Digital Operational Resilience Act (DORA) & ICT Risk Management

DORA enforcement began January 17, 2025, requiring EU financial entities to demonstrate comprehensive ICT risk management, including continuous testing, incident response playbooks, and third-party risk oversight, particularly for critical cloud providers.

DORA demands complete traceability through your technology supply chain: which systems handle critical functions, what data flows to third parties, how quickly can you recover from disruptions, and where are concentration risks hiding? Regulators globally continue to implement regulatory changes and programs of work to ensure that financial institutions meet the resilience challenges of a digital age. DORA requires banks to answer questions like: Which applications handle payment processing? If your primary cloud provider experiences an outage, which business functions are affected? Where does customer data flow to third-party processors? How quickly can you restore critical systems after a cyber incident?

Data lineage and system cataloging provide the foundation for answering these questions. Without visibility into how data flows through your technology stack, DORA compliance becomes guesswork.

7. EU T+1 Settlement Data Readiness

The EU's T+1 settlement roadmap targets phased go-live starting December 2026 through October 2027. This compression from T+2 to T+1 requires intraday data timeliness, automated breaks management, and real-time funding forecasts (capabilities depending on near-real-time data integration across trading, clearing, custody, and treasury systems).

Can your settlement systems reconcile trades, allocations, and confirmations fast enough? Do you have real-time visibility into settlement obligations, cash positions, and collateral requirements? Legacy batch processing and end-of-day reconciliation won't suffice.

8. AI Governance Under the EU AI Act

The EU AI Act, passed in 2024, classified financial services models used in credit scoring, KYC, and fraud detection as "high-risk," triggering stricter requirements on training data governance, bias mitigation, and audit logging.

High-risk AI obligations take effect August 2, 2026: What training data was used? How was data quality validated? Can you explain how the model reached specific decisions? What controls prevent discriminatory outcomes?

Financial institutions must maintain audit trails showing data provenance, model versioning, validation results, and ongoing monitoring. When a regulator questions a credit decision made by your AI model, can you trace it back to specific training data and model parameters?

9. Cross-Border Data Governance and International Data Transfers

Banks operating internationally must navigate GDPR's strict requirements for transferring personal and financial data outside the EU. The Schrems II ruling invalidated the EU-U.S. Privacy Shield, forcing banks to implement supplementary measures and case-by-case assessments for transatlantic data transfers.

Financial institutions must maintain visibility into where customer data resides, how it moves across borders, which legal basis authorizes each transfer (standard contractual clauses, binding corporate rules), and how retention periods vary by jurisdiction.

Without proper data classification and lineage tracking, banks can't prove which data crossed which borders under which legal mechanisms.

In addition to these nine regulatory compliance challenges, there is one more related to the adoption of AI agentic systems:

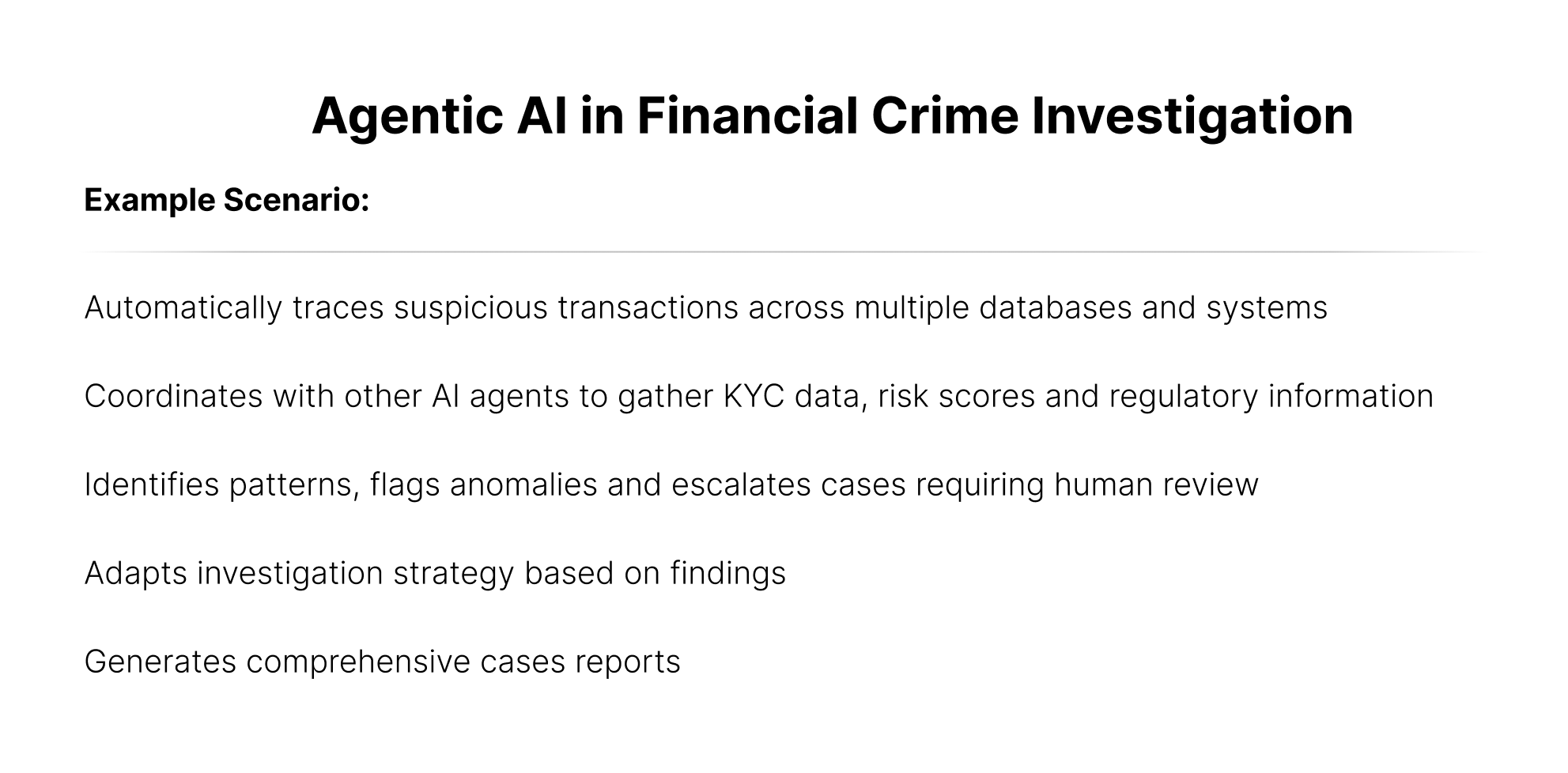

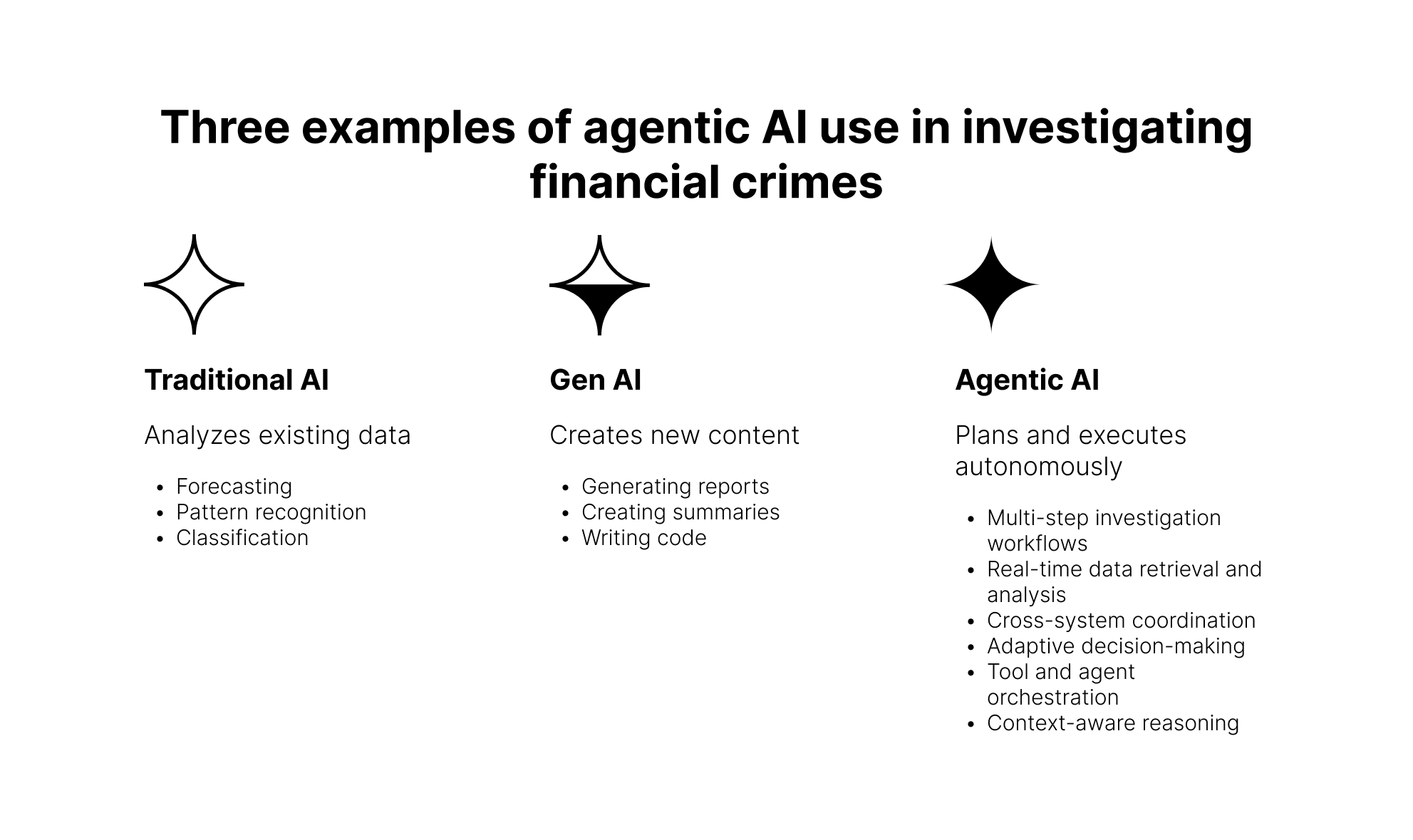

AI Agent Readiness: When Conversational Analytics Need Business Context

Financial institutions are rapidly adopting AI agents for fraud prevention, financial crime investigation, and regulatory compliance. These agentic systems can autonomously trace suspicious transactions across multiple databases, gather KYC data and risk scores, identify patterns requiring human review, and generate comprehensive case reports.

But AI agents are only as reliable as the business context they access. When an agent investigates potential money laundering, does it understand that "customer" means different things in your CRM versus trading systems? Can it distinguish between gross and net exposure? Does it know which data sources are authoritative for AML reporting?

Banks are employing AI agents that collaborate to perform end-to-end tasks autonomously, with humans only required for exception handling and oversight. Analyzing the effects of using multi-agent systems showed productivity gains of 20 to 60 percent, but only when systems have access to properly contextualized data.

Through Model Context Protocol (MCP), AI agents can access not just raw data but the semantic layer defining business meaning: unified glossaries, data lineage, business rules, and quality indicators. Without this context, conversational analytics generates unreliable answers, undermining trust and creating compliance risk.

As CFOs demand metrics, analytics, and reporting as their top priority, they're discovering that AI agents need the same unified business context that human analysts require. The question isn't whether to deploy AI agents, it's whether your data foundation can support them reliably.

The Data Governance Foundation Banks Need

Leading financial institutions are building modern data governance infrastructure that automates compliance and provides complete visibility across all data systems. Key capabilities include:

- End-to-end automated lineage connecting source systems through transformations to regulatory reports (maintained continuously, not assembled during audits).

- Unified business glossary ensuring "customer," "transaction," and "exposure" have consistent definitions across systems, with explicit mappings to regulatory requirements.

- Policy-to-control-to-data mapping showing which regulations require which data elements and which reports demonstrate compliance.

- Impact analysis answering "If this source system changes, which regulatory reports are affected?" in seconds rather than weeks.

- Immutable audit trails capturing who accessed what data when, which transformations were applied, and how business rules evolved. Audit-ready evidence without manual documentation.

- Role-based access and jurisdiction-aware retention enforcing GDPR and local requirements automatically based on data classification.

Why Financial Services Can't Wait

CFOs and finance leaders rate metrics, analytics, and reporting as their top focus area for 2025, reflecting an emphasis on delivering insight to improve business performance. The convergence of regulatory complexity, AI governance requirements, operational resilience mandates, and cross-border data protection creates unprecedented pressure on data foundations.

Spreadsheets weren't designed for DORA's continuous testing or explaining AI credit decisions. Manual data management can't keep pace with hundreds of daily regulatory changes. Legacy data governance (documenting relationships once during implementation) becomes obsolete as business processes, systems, and regulations constantly evolve.

When your next regulatory examination begins, the question shouldn't be "Where do we start gathering evidence?" It should be "Which report do you want to see first?", with complete lineage, ownership, controls, and audit trails available instantly.

Continue scaling manual processes to meet accelerating regulatory complexity, or build the automated data governance infrastructure that makes compliance sustainable. 2026 will reveal which path your organization has chosen.